California Climate Disclosure Countdown

Regulation for Implementation of SB 253 / Health & Safety Code § 38532

On May 20, 2026, the California Air Resources Board ("CARB") submitted its initial regulation implementing the California climate disclosure laws to the Office of Administrative Law ("OAL") for review. Because OAL still has the CARB rulemaking under review, on June 24, 2026, CARB announced that it intends to defer the first-year reporting deadline under SB 253 for Scope 1 and Scope 2 greenhouse gas (“GHG”) emissions from August 10, 2026, to November 10, 2026. The three-month deferral will be proposed as part of a forthcoming package of limited regulatory changes that CARB intends to release for a 15-day public comment period.

While SB 253 creates a statutory obligation, the regulation supplies the mechanics—definitions, fees, recordkeeping, and deadline. Until OAL acts, companies occupy an unusual middle ground: the statute points toward 2026 reporting, but the rule establishing the compliance details is not yet effective. This makes the newly proposed November 10, 2026, date the new working target, rather than a settled deadline.

The immediate planning issue is preparing for Scope 1 and Scope 2 GHG emissions reporting under SB 253. Scope 3 reporting begins in 2027 on a schedule CARB will specify. SB 253 includes a safe harbor for Scope 3 misstatements made with a reasonable basis and disclosed in good faith, and from 2027–2030 limits Scope 3 penalties to non-filing.

Ongoing litigation adds uncertainty. In Chamber of Commerce v. Sanchez (9th Cir. No. 25-5327)—a First Amendment challenge to SB 253 and SB 261—the Ninth Circuit enjoined SB 261 pending appeal but declined to enjoin SB 253. Oral argument occurred January 9, 2026. SB 261's narrative climate-risk disclosures drew particular scrutiny; SB 253's quantitative Scope 1 and 2 disclosures appeared to face less pressure, though Scope 3 also raised concerns. No ruling has been issued yet.

What the Initial Regulation Does—and Does Not Do

CARB's initial regulation addresses definitions, recordkeeping, fee mechanics, and the first-year reporting deadline. It does not establish the full reporting program—templates, assurance details, and recurring deadlines will come in subsequent rulemakings.

Three practical clarifications from CARB's final materials:

- Applicability is assessed entity-by-entity. A subsidiary's revenue is not automatically attributed to a parent, and vice versa.

- Parent reporting does not eliminate subsidiary fees. A parent may report for an in-scope subsidiary, but the subsidiary retains its own fee obligation if it independently meets the criteria.

- Estimated fees—roughly $3,100 per SB 253 reporting entity and $1,400 per SB 261 covered entity—are not fixed in the rule. The regulation uses formulas based on program costs and the number of in-scope entities. Once fee notices are issued, payment is due within 60 days.

Recordkeeping

For companies near the $1B threshold or with complex structures, contemporaneous documentation is prudent to build a defensible compliance record.

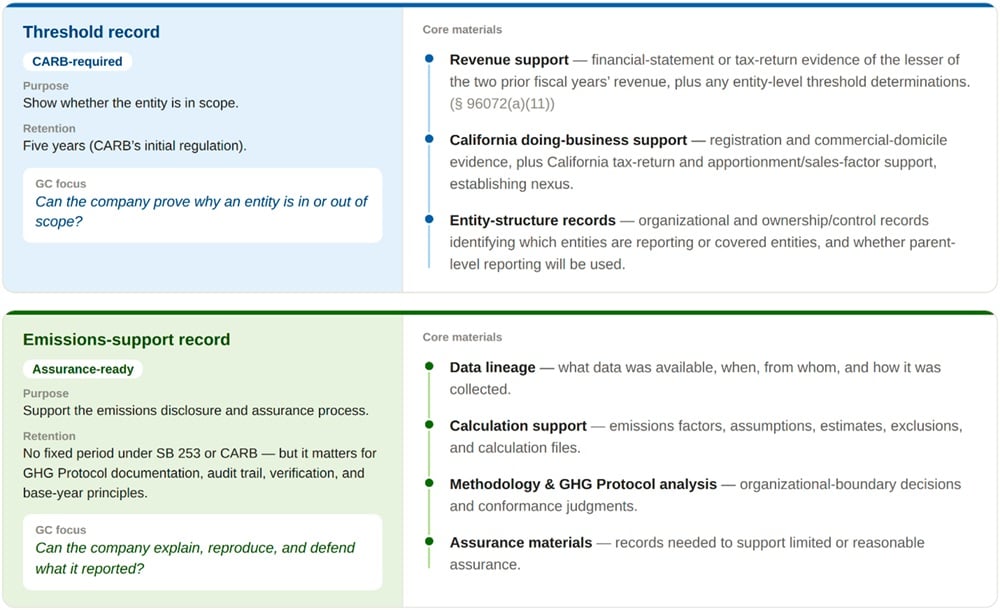

CARB's initial regulation requires five-year retention of records demonstrating an entity meets the applicable revenue and California doing-business thresholds. Although § 96074(d) applies to in-scope entities, documenting out-of-scope status is also prudent for near-threshold entities. Because these records must be produced to CARB on request, underlying factual support should be kept separately from any privileged scoping analysis to avoid waiver on production.

That threshold record should be distinguished from SB 253's separate obligation to measure and report emissions in conformance with the GHG Protocol and obtain assurance. The GHG Protocol addresses documentation, archiving, audit trail, verification, and base-year support, but does not prescribe a fixed retention period for methodology papers, emissions factors, data lineage, or calculation files.

Practically, it means companies should consider maintaining two related but distinct categories of records.

The core compliance steps—scoping, emissions data collection, framework alignment, assurance preparation, and drafting—take time. Companies should consider continuing to build compliance infrastructure while monitoring the ongoing litigation challenging the rules.