How Long Does Australian FIRB Approval Take? Latest Statistics and More Streamlining Reforms

In Short

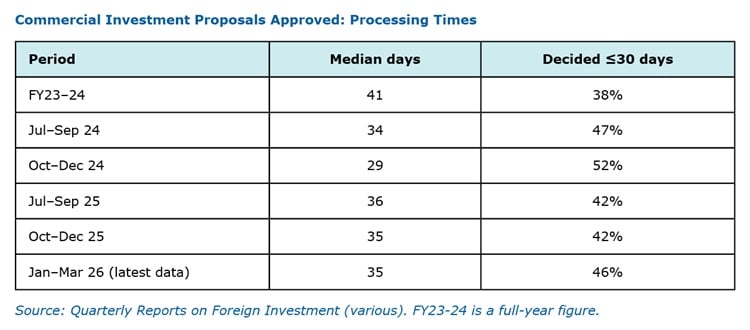

The Background: Under Australia's foreign investment legislation, the Treasurer has 30 days to consider a foreign investment proposal, and a further 10 days to notify the outcome, subject to the review period being extended. Since 1 January 2025, Treasury has targeted deciding 50% of commercial proposals within that 30-day window.

The Result: Treasury's latest quarterly data shows a median processing time of 35 days, with 46% of proposals decided within 30 days. This was amidst a material increase in foreign investment value for Q1 2026, despite an over 10% fall in application numbers.

How Long Does FIRB Approval Take: What the Data Shows vs a Practical Perspective

Under section 40 of the Foreign Acquisitions and Takeovers Act 1975 (Cth) ("FATA"), the Treasurer has 30 days to consider an application, and a further 10 days to notify of the outcome. If no decision is made within that period (and the period has not been extended), the application is taken to be approved under FATA.

In practice, where the Foreign Investment Review Board ("FIRB") requires more time, it will request the applicant to voluntarily extend the decision period or will otherwise unilaterally extend the decision period by up to 90 days. While FIRB has generally improved approval timeframes, Treasury's target of deciding 50% of commercial proposals within 30 days has proven difficult to sustain. After a brief improvement in late 2024, the median processing period has returned to 35 days.

Although Treasury does not provide data on processing times by application type, notifiable national security actions—a subset of commercial proposals—draw more heavily on FIRB's resources and can extend approval timeframes. Investors pursuing these types of investments should continue to plan for longer review periods.

New Streamlining Reforms: What Is Changing and Why It Matters

Building on its 2024 reforms, in mid-May, the government announced a further package aimed at speeding up low-risk FIRB reviews and strengthening the process for higher-risk proposals. Key elements (noting these are not yet law) include:

Low-risk pathway and a new performance target

- New performance target from 1 January 2027 for all 'low risk' applications to be decided within 30 calendar days.

- Streamlining measures to reduce burden for clearly 'low risk' transactions and experienced, compliant investors.

Stronger tools for higher-risk cases

- Enhanced powers to tailor conditions, including pre-acquisition conditions, accept undertakings and issue more flexible orders and directions.

- An expanded toolkit to address influence-based association arrangements, for example, certain debt, offtake or other non-ownership controls, and to tighten anti-avoidance provisions.

Targeted changes to scope and process

- Adjustments to notification settings and exemptions to focus on control and material influence.

- Greater flexibility around approvals, for example, validity periods, expanded scope for exemption certificates and a more pragmatic approach to legacy, low-value conditions.

Streamlined reporting to the Register of Foreign Ownership of Australian Assets

- Reducing duplicate notifications to the Register of Foreign Ownership of Australian Assets (for actions already approved by FIRB).

- Reporting will continue for specified asset classes, including residential land, agricultural land, certain mining tenements and water interests.

What Is a Low-Risk Application?

To be considered low risk, an application will need to be made by a foreign person who has received FIRB approval in the past 24 months, has no record of non-compliance or character concerns and is not subject to extrajudicial direction.

The proposed action must also not be in a sensitive sector or business (which would include a national security business), have no national security sensitivities and has a straightforward and transparent corporate structure.

Despite these categorisations, assessment timeframes for investors pursuing national security investments, investments into sensitive sectors, such as critical minerals, sensitive data or critical technology or with complicated fund structures, will likely remain in excess of 30 days.

Clarifying the Interrelationship Between Mandatory ACCC Regime and the FIRB Approval Process

With Australia's mandatory competition filing regime now in place, Treasury has confirmed that FIRB approval will not be given prior to ACCC approval where both are required. Treasury will seek to align decision dates where possible.

Adjustments to Upstream Tracing Rules

Under the proposed reforms, the upstream tracing rules, which currently deem any owner of 20% or more of an entity (together with their associates) as holding a 100% interest in any downstream entity or business, will be amended to instead focus approval requirements on instances where upstream ownership gives rise to material interests or control. These adjustments to the tracing rules, especially if applied to foreign government investors, will likely have significant ramifications as to whether transactions, especially global transactions, require FIRB approval.

Broader Exemption Powers, but Expanded Mandatory Approval Requirements for Sensitive Sectors

The reforms will empower the Treasurer to effectively 'turn off' or otherwise adjust the application of various rules, including whether an investor is classified as a foreign government investor and the application of the tracing and association rules. If implemented, these adjustments may enable frequent inbound investors, which are classified as foreign government investors due to passive upstream ownership interests, to avoid the onerous obligations placed on them by Australia's foreign investment regime.

While the reforms propose to completely exempt certain low-risk transactions from the approval requirements, including where a minor change in ownership occurs without any control implications, the reforms would expand mandatory approval requirements for investments into sensitive sectors. While no such sensitive sectors have been named, we expect these to include critical minerals, including rare earth elements, critical technologies and potentially investments into critical data storage and processing assets, such as data centres.

Other Recent Treasury Data: What Are the Key Sources of Recent Foreign Capital Inflows and Most Popular Sectors?

Treasury's Q1 2026 statistics show Singapore led by value (AU$16.0 billion, up from AU$1.4 billion), followed by the United States (AU$12.5 billion) and the United Arab Emirates (AU$10.1 billion, up from AU$1.9 billion). Headline flows reflect fund-led activity and Singapore's role as a hub for global capital investing into Australia.

By sector, 'services' remained largest by value, followed by commercial real estate and manufacturing, electricity and gas.

Three Key Takeaways

- Treasury's 30-day performance target now applies only to low-risk applications. In practice, this low-risk categorisation is unlikely to materially shorten timeframes for more complex investments.

- A range of the other streamlining measures are positive developments, particularly with respect to the upstream tracing rules. However, the further mandatory approval requirements to be applied to sensitive sectors, introduction of new powers to extend conditions to the pre-acquisition period, statutory undertakings and other powers to make orders and directions will add complexity to the regime.

- The alignment of FIRB and ACCC processes for transactions requiring both approvals provides welcome clarity for investors navigating Australia's dual regulatory pathways.