.jpeg?rev=a4fb8eaa4c664b699b4777701b72825e&la=en&h=800&w=1600&hash=0302DCCBD7C59663666B451AD1C6B393)

Final Disclosure Recommendations From the Taskforce on Nature-related Financial Disclosures

On September 18, 2023, the Taskforce on Nature-related Financial Disclosures ("TNFD") released its final recommendations for disclosures on nature-related dependencies, impacts, risks, and opportunities. The TNFD aims to tackle nature and biodiversity loss and make it easier for investors to identify those companies that align with their values vis-à-vis the natural world.

Natural capital and biodiversity are gaining prominence in the public and private sector. Many expect the recommendations to raise the profile of nature-related issues in the same way that the Taskforce on Climate-related Financial Disclosures ("TCFD") proved to be the catalyst for both voluntary and mandatory climate-related disclosures. For example, in the United Kingdom, the TCFD-recommended disclosures have now become a key element in the regulatory landscape.

For this reason, companies should take note of the TNFD recommendations and begin to consider whether their organization needs to develop a strategy on natural capital and biodiversity.

The TNFD recognizes that declines in nature compromise our ability to mitigate climate change, and similarly nature can be harnessed to help combat climate change and its effects. In this respect, nature should be viewed as a core and strategic risk management issue alongside climate change. As such, the TNFD recommendations follow a similar framework to the TCFD, only reframed to include natural capital and biodiversity. As such, the disclosures follow the same four pillars of governance, strategy, risk and impact management, and metrics and targets. Whereas the TCFD is focused solely on disclosure of climate-related risks and opportunities, the TNFD recommendations encourage companies to produce integrated climate-nature disclosures and to develop appropriate risk management processes to address climate-nature risks.

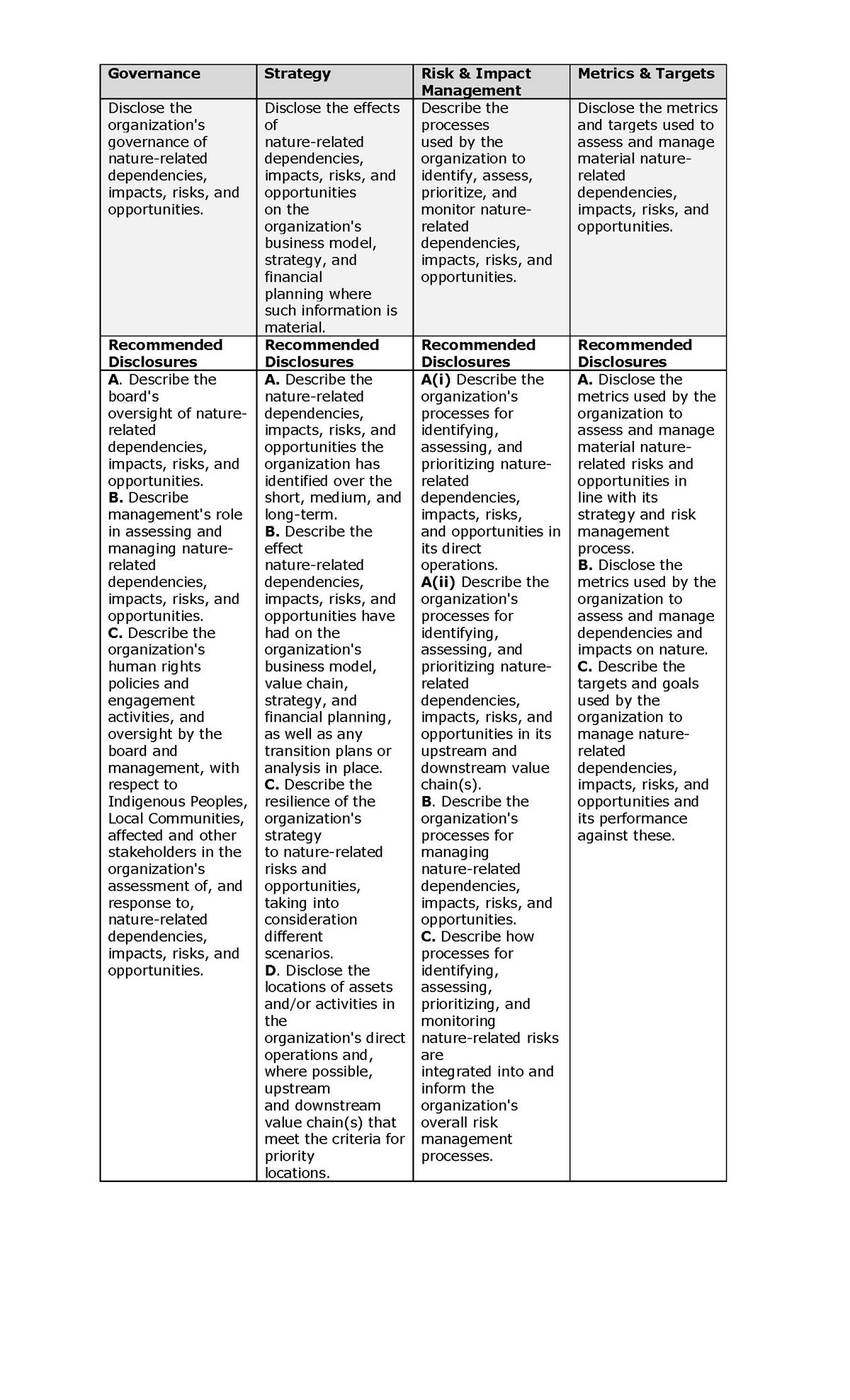

The 14 TNFD recommended disclosures include the 11 TCFD-recommended disclosures (but recast for nature) and add a further three disclosures relating to: (1) stakeholder rights and engagement; (2) priority locations; and (3) value-chain risk and impact management. The full recommended disclosures are set out in Table 1 below.

A number of guidance documents have been published alongside the final recommendations. This includes guidance to assist organizations with the necessary due diligence to inform their nature-related strategy and disclosures. Part of this is the "LEAP" process, which is mnemonic for a four-step process: (1) Locate the interface with nature; (2) Evaluate dependencies and impacts on nature; (3) Assess nature-related risks and opportunities; and (4) Prepare to respond to nature-related risks and opportunities and to report on these.

Further guidance is provided on metrics and targets, acknowledging that, unlike the role of greenhouse gas emissions for climate change, natural capital is not as straightforward to gauge. As such, the guidance breaks down the metrics into a number of "indicators," including total spatial footprint; extent of land/freshwater/ocean-use change; pollutants released to soil; wastewater discharged; waste generation and disposal; plastic pollution; non-GHG air pollutants; water withdrawal and consumption from areas of water scarcity; quantity of high-risk natural commodities sourced from land/ocean/freshwater; value of assets, liabilities, revenues, and expenses assessed as vulnerable to nature-related transition risks and nature-related physical risks; description and value of significant fines/penalties received/litigation action in the year due to negative nature-related impacts; amount of capital expenditure, financing, or investment deployed toward nature-related opportunities; and increase and proportion of revenue from products and services producing demonstrable positive impacts on nature, with a description of impacts.

The TNFD will track voluntary market adoption on an annual basis through an annual status update report beginning in 2024. An inaugural list of TNFD Adopters will be announced at the World Economic Forum at Davos in January 2024, and it is expected that many high-profile companies will feature as early adopters.

Table 1. TNFD-Recommended Disclosures

Companies with questions regarding the TNFD should consult with experienced counsel.