Both Convergence and Divergence Seen in Emerging State Climate Disclosure Bills

Although the federal Securities and Exchange Commission has stayed its 2024 climate-related disclosure rule, certain U.S. states continue to advance their own climate-related disclosure legislation. California's landmark Senate Bills 253 and 261 ignited a wave of copycat or companion proposals in New York, Colorado, New Jersey, and Illinois. These state bills share a common architecture yet differ in several material respects that will shape compliance strategy.

If these laws are enacted, they may be challenged as preempted by federal law or otherwise unconstitutional. This tension is particularly prominent given negative treatment of state climate laws in President Trump's executive orders. In addition, recent rulings in climate nuisance cases suggest that regulation of greenhouse gas ("GHG") emissions presents questions for federal, rather than state, courts.

Nonetheless, it is useful to monitor how states are proceeding because it may form something of a template for federal laws and regulations in a future administration. In addition, recent attempts by some business groups to halt these bills—specifically California's SB 253 and SB 261—have fallen flat, suggesting their "end" is not soon forthcoming. Specifically, on August 13, 2025, the United States District Court for the District of Central California denied the U.S. Chamber of Commerce's and other business groups' request for a preliminary injunction to pause California's two disclosure bills. The takeaway: Despite tension with the federal government, companies should remain up to date on the status, contours, and requirements of these state bills.

Common Architecture

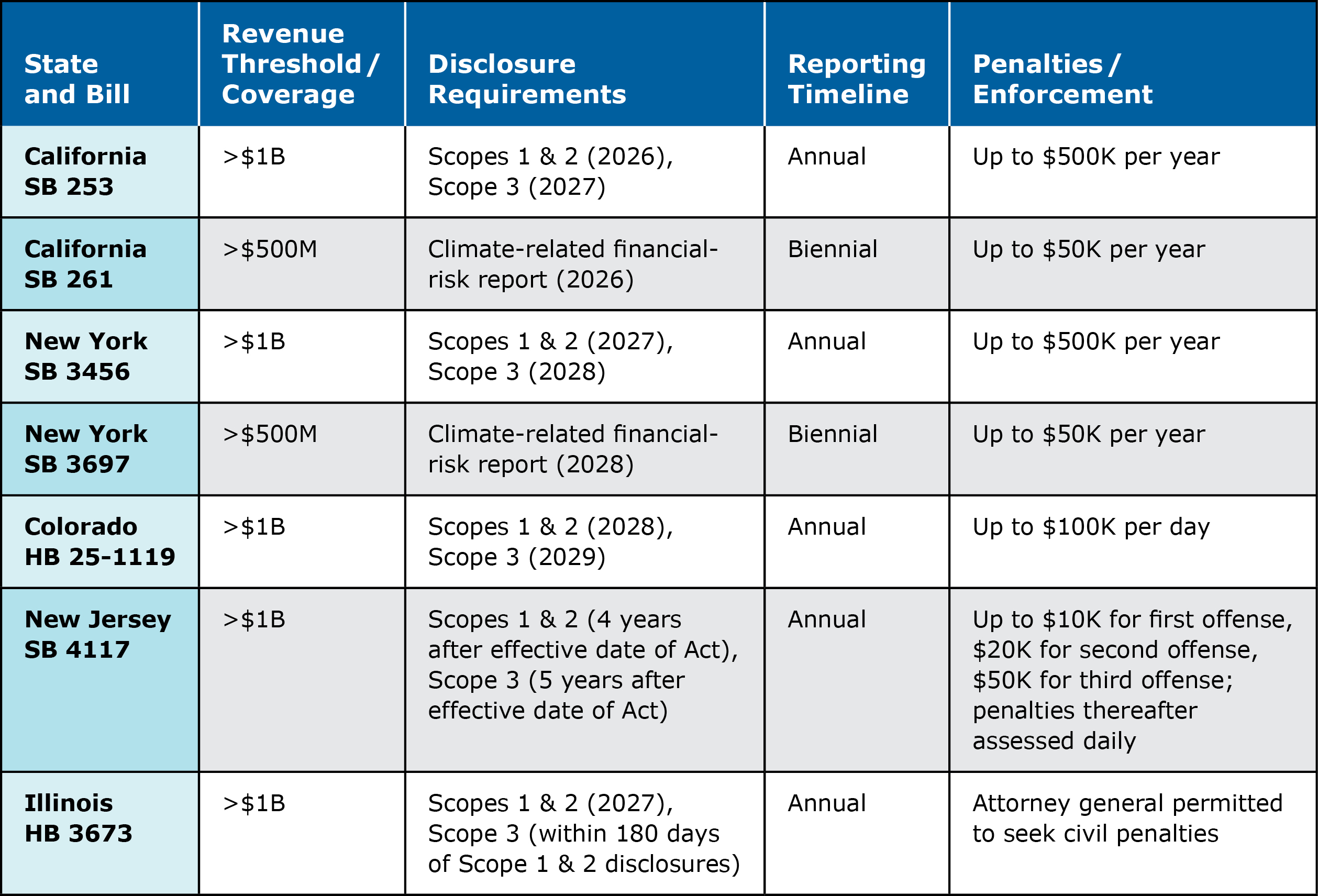

- Revenue Threshold of $1 Billion (or $500 Million for Risk Reports). The trigger for the emissions reporting bills is total annual revenue "in excess of one billion dollars" earned by the entity and its subsidiaries while "doing business" in the state. California's SB 261 (financial risk-reporting bill) and New York's separate risk-reporting bill (SB 3697) adopt a lower $500 million threshold, expanding coverage to more companies. It is not clear in all instances if the revenue threshold is judged by enterprise-wide revenue or only the revenue of entities that do business in the reporting jurisdiction.

- Mandatory Scope 1, 2, and 3 Emission Inventories. All bills require disclosure of direct (Scope 1), energy-indirect (Scope 2), and value-chain (Scope 3) emissions, although timing and granularity differ. The bills uniformly require use of the Greenhouse Gas Protocol Corporate Accounting Standard ("GHG Protocol") and Corporate Value Chain Standard, ensuring at least technical harmonization.

- Third-Party Assurance—Limited First, Reasonable Later. Verification by an independent assurance provider is a defining element. Most bills start with limited assurance for Scopes 1 and 2 (California 2026; New York 2027) before escalating to reasonable assurance after a multiyear runway (California 2030; New York 2031).

- Public-Facing, Fee-Funded Registries. Each state contemplates filing emissions data with, and often paying fees to support, a designated agency or nonprofit that will publish a searchable database. California assigns that duty to the California Air Resources Board ("CARB"); New Jersey gives the role to a nongovernmental organization selected by the New Jersey Department of Environmental Protection.

Points of Divergence

- Scope 3 Phase-In Designs. Bills split over whether to require full Scope 3 disclosure on a single date or to stage reporting by category. New York and Colorado adopt a stepped approach: limited upstream categories in year one, expanding to downstream categories in subsequent years.

- Risk-Reporting Layer. Only California's (SB 261) and New York's (SB 3697) risk bills mandate biennial climate-related financial risk reports aligned with the Task Force on Climate-related Financial Disclosures. Other states focus solely on quantitative emissions.

- Free-Speech Exemption. Colorado uniquely allows companies to withhold information if disclosure would violate the U.S. or state constitutions' free-speech guarantees, subject to advance notice to the attorney general.

- Penalty Levels and Enforcement. California imposes civil penalties up to $500,000 per reporting year for missing or materially misleading emissions data (SB 253) and $50,000 for financial risk reports (SB 261). Colorado authorizes fines of up to $100,000 per day, signaling a more aggressive deterrent. New Jersey sets escalating penalties from $10,000 to $50,000 per offense, plus daily fines. Illinois remains silent, leaving penalty caps to later rulemaking.

- Legislative Status. California's statutes are enacted but under litigation; regulations were due by July 1, 2025, but at this point have not been proposed. However, it is important to note that: (i) despite the potential for continued litigation, the deadline for first reports remains on track for 2026, given the recent preliminary injunction denial by the United States District Court for the District of Central California; and (ii) despite delaying the original July 2025 deadline, CARB is aiming to release regulations in 2026.

Other bills are pending—New York in Senate Committee, New Jersey in Budget and Appropriations, Illinois in Rules Committee. Colorado's bill, meanwhile, has been postponed indefinitely; however, it is expected to be reintroduced in the next legislative session. Companies therefore face a moving target with uneven certainty across jurisdictions.

Strategic Takeaways

- Plan for California Compliance First. Because every other state thus far explicitly borrows from, or allows compliance via, California reports, building a California-ready GHG inventory is the most efficient hedge against multistate exposure.

- Strengthen Data Governance for Scope 3. Differences in phase-in schedules matter far less than the underlying need to collect supplier, customer, and employee activity data. Establishing contractual data-sharing clauses across the value chain will prove critical.

- Monitor Litigation and Federal Preemption. The potential for continued litigation challenging California's legislation, combined with President Trump's April 2025 executive order targeting state climate laws, could alter enforcement timelines. Nevertheless, the political trend suggests at least some state requirements will survive, and voluntary reporting may become a de facto investor expectation regardless of legal outcomes.

- Budget for Assurance. Limited-assurance engagements must commence as early as fiscal-year 2025 in California. Selecting auditors with both GHG expertise and independence credentials now will avoid capacity bottlenecks.

The table below consolidates the principal similarities and differences for quick reference:

In sum, while each state bill contains idiosyncrasies, their collective architecture signals an emerging "California-plus" model. Multistate enterprises that operationalize robust, GHG Protocol-aligned data systems, engage third-party assurance partners, and stay attuned to litigation risks will be best positioned to navigate this rapidly evolving patchwork.

Read the full Climate Report.