U.S. Banking Agencies Propose Sweeping Overhaul of Capital Framework - Part III: Category II Banking Organizations

In Short

The Situation: On March 19, 2026, the OCC, Federal Reserve, and FDIC proposed to modernize capital requirements by mandating ERBA for Category I–II organizations, eliminating advanced approaches, dropping the standardized approach for these firms, revising market risk and introducing standardized operational risk capital, and applying CVA to Category I–II and a narrow set of high‑activity banks; comments are due June 18, 2026.

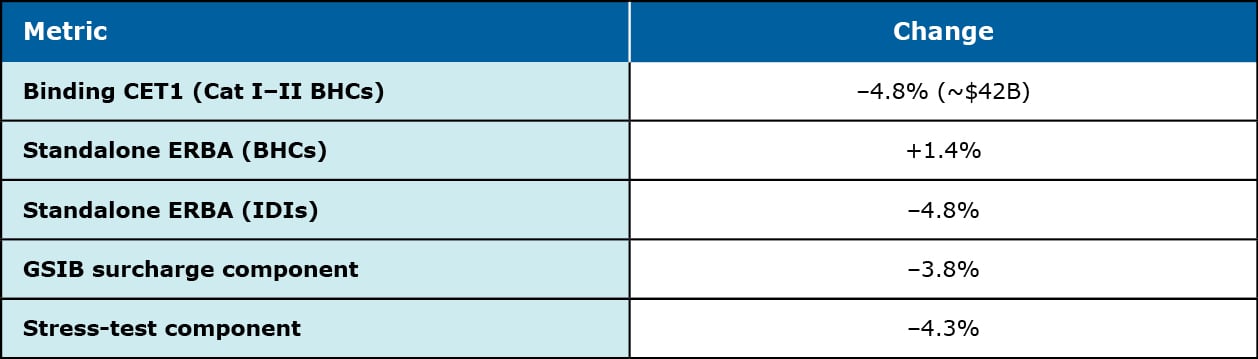

The Bottom Line: For Category II banks, ERBA becomes the binding single stack, with explicit operational risk capital and activity‑based market risk and CVA, alongside continued AOCI recognition and a shift of MSAs from deduction thresholds to a uniform 250% risk weight; in combination with the GSIB surcharge proposal and stress test changes, aggregate CET1 requirements for Category I–II bank holding companies are projected to fall by approximately 4.8%, but firm‑level effects will hinge on trading intensity, retail‑credit mix, and mortgage‑related exposures.

Looking Ahead: Indexed thresholds, a three‑year transition for the new market risk PLA test, and anticipated stress‑testing recalibrations suggest a multiyear implementation period in which trading‑book and CVA dynamics are materially offset for some banks by stress‑test changes, while consolidation and optional ERBA uptake by non‑Category II peers may alter competition.

Scope and Structural Changes for Category II Banks

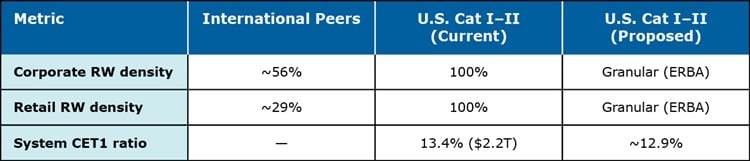

- ERBA is the only set of capital requirements for Category II organizations, eliminating dual‑stack calculations. The current standardized approach no longer applies to these firms, and the second capital calculation under the advanced approaches is removed. All other banking organizations may opt into ERBA.

- ERBA increases risk‑sensitivity through standardized methodologies for credit, equity, and operational risk, while leaving market risk internal models available (with approval) and simplifying core design relative to legacy internal‑model constructs.

- The agencies intend single‑stack ERBA to reduce overlap with stress testing and to align U.S. capital requirements more closely with international standards, while providing optionality for non‑Category II firms and preserving AOCI treatment for those adopting ERBA.

Quantified Capital Impacts for Category II Holding Companies and Depository Institutions

The standard deviation across the nine Category I–II bank holding companies is approximately 8.7%, indicating individual outcomes will diverge substantially from the aggregate. Banks' individual outcomes will depend on a number of factors, including trading activity and extent of mortgage operations.

Credit Risk Under ERBA: Granularity and Mortgage‑Related Effects

Framework refinements:

- Off‑balance sheet conversion factors

- An expanded suite of credit risk mitigants

- Revisions to standardized approach to counterparty credit risk (SA‑CCR) for SFT/derivatives netting

- Revisions to a standardized securitization approach with U.S.‑specific adjustments

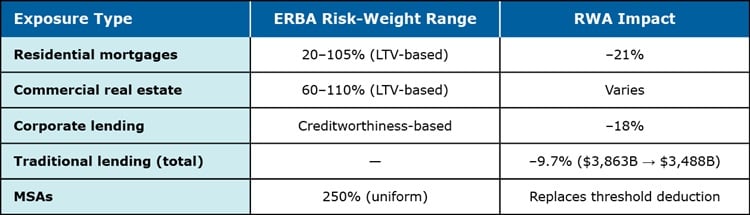

- MSA treatment: The removal of the threshold‑based MSA deduction in favor of a uniform risk weight reduces cliff effects and disincentives for mortgage origination and servicing—particularly relevant to Category II lenders with significant mortgage platforms.

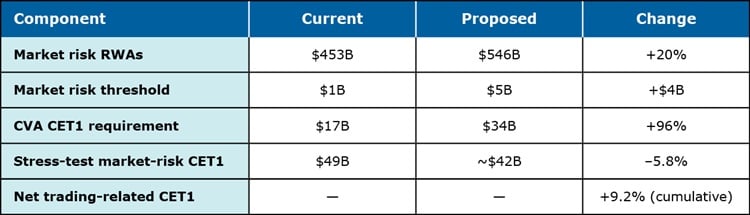

Trading, Market Risk, and CVA: Applicability, Methods, and Offsets

- CVA applicability: Extends to Category II holding companies and depositories with significant trading activity, plus other firms with ≥$1 trillion in notional derivatives; basic CVA and SA‑CVA methods are available.

- PLA transition: A three‑year phase‑in for the profit‑and‑loss attribution test avoids immediate automatic consequences—operationally important for Category II firms managing model upgrades and desk‑level validation.

Operational Risk Capital: Standardization and Interplay With Stress Testing

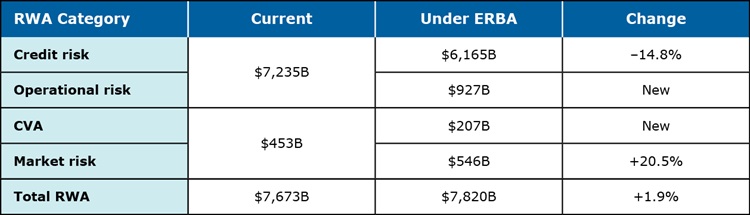

- Operational risk RWAs for Category I–II holding companies would total approximately $927 billion under ERBA, representing a significant structural addition, as the current framework includes no explicit operational risk charge. The standardized charge depends on business volume, with a 70% reduction in income contributions from investment management, investment services, and non‑lending treasury services.

- The Federal Reserve's 2025 stress‑testing revisions are expected to lower stress capital buffer components related to operational loss projections, explicitly aiming to offset ERBA's standalone increases.

Capital Definition, AOCI, and Disclosure Implications

- AOCI: Category II banks would continue to reflect most elements of AOCI in CET1; any bank opting into ERBA must adopt the Category I–II capital definition, including AOCI treatment.

- Disclosures: Enhanced public disclosures currently applicable to Category I–II carry forward under ERBA, with top‑tier holding‑company scope and new or refined tables to improve transparency.

- While a new TLAC‑instrument disclosure table applies specifically to Category I, Category II organizations will face broadened narrative and quantitative disclosures across credit, counterparty, market, CVA, and operational risk.

Timing, Thresholds, and Implementation

- Comments are due June 18, 2026; the agencies solicit views on effective dates and phased implementation.

- Dollar‑based thresholds—including trading‑activity thresholds—would be indexed to inflation and adjusted every two years, an important dynamic for Category II firms near activity cutoffs.

- FFIEC reporting forms will be aligned with ERBA's measurement architecture, requiring systems and process changes at Category II organizations.

- The agencies acknowledge overlaps with stress testing, noting that reductions in modeled operational‑ and market‑risk stresses under the Board's 2025 proposals are intended to balance ERBA's standardized capital increases.

Competitive and Strategic Implications for Category II Banks

- Product‑specific market‑risk changes could shift incentives for liquidity provision between banks and nonbanks.

- Stress‑testing changes are designed to mitigate procyclicality.

- The agencies link calibrated capital reductions to a policy environment more receptive to large‑bank consolidation. More Category I–II firms could emerge under enhanced prudential standards, with agency support for merger activity—a factor Category II boards should weigh in inorganic growth strategies.

Five Key Takeaways

- Single‑stack ERBA is now mandatory for Category II banks. Advanced approaches and the current standardized approach are eliminated; market risk and CVA apply by rule, with basic and SA‑CVA methods available.

- Net CET1 relief is projected at approximately 4.8% for Category I–II bank holding companies when ERBA is combined with the GSIB surcharge proposal and stress‑test changes—but outcomes will vary significantly by trading intensity and portfolio mix.

- Operational and market‑risk capital increases under ERBA are designed to be offset by anticipated stress‑testing revisions; firms should model both regimes together when assessing true capital impact.

- Credit‑risk granularity and MSA reforms create optimization opportunities in traditional lending and servicing; systems, data, and reporting workstreams for enhanced ERBA disclosures should begin promptly.

- Boards should reassess capital planning, portfolio allocation, and M&A strategy in light of a policy environment that could produce more Category II peers and favors large‑bank consolidation. Comments are due June 18, 2026.