ISS Issues 2017 Summary Proxy Voting Guidelines

On December 22, 2016, ISS published its 2017 Summary Proxy Voting Guidelines, which will be effective for shareholder meetings on or after February 1, 2017. This Commentary provides an overview and summary of the changes made from the proxy advisory firm's 2016 Guidelines.

Problematic Takeover Defenses

ISS now recommends a vote against or withhold from members of the governance committee if the company's charter unduly restricts shareholders' ability to amend the bylaws. ISS includes the following in a nonexclusive list of undue restrictions:

- Outright prohibitions on the submission of binding shareholder proposals, and

- Share ownership requirements or time holding requirements in excess of SEC Rule 14a-8.

Under Rule 14a-8, shareholders may include proposals in the company's proxy statement as long as they meet certain eligibility and procedural requirements. The shareholder must own at least $2,000 in market value, or 1 percent, of securities entitled to vote on the proposal for at least one year before the date the proposal is submitted to the company, and he or she must hold the securities through the date of the annual meeting.

Problematic Capital Structures

ISS has also added guidelines addressing what it considers to be problematic capital structures in newly public companies. ISS will recommend a vote against or withhold from directors individually, committee members, or the entire board (except new nominees, who should be evaluated on a case-by-case basis) if, prior to or in connection with the company's public offering, the company or its board implemented a multi-class capital structure in which the classes have unequal voting rights. This determination is based on a consideration of multiple factors:

- The level of impairment of shareholders' rights,

- The disclosed rationale,

- The ability to change the governance structure,

- The ability of shareholders to hold directors accountable through annual director elections or whether the company has a classified board structure,

- Any reasonable sunset provision, and

- Other relevant factors.

As was the case in its 2016 Guidelines, the foregoing analysis and recommendation also applies to a company or board that has adopted bylaw or charter provisions materially adverse to shareholder rights.

Overboarded Directors

Starting in 2017, ISS will issue a negative recommendation for directors who sit on more than five public company boards. Historically, ISS has advised a vote against or withhold from directors who sit on more than six public company boards, but last year it announced that, starting in February of 2017, the threshold number of boards would be reduced to five. ISS will continue to vote against or withhold from an individual director who is the CEO of a public company who sits on the board of more than two public companies besides his or her own.

Share Issuance Mandates

Also new in 2017 is a recommendation to vote in favor of general share issuance authorities (without a specified purpose) without preemptive rights to a maximum of 20 percent of current issued capital, as long as the company clearly discloses the duration of the authority and such authority is reasonable. ISS suggests that companies should seek renewal of the issuance authority at each annual meeting.

Equity-Based and Other Incentive Plans

ISS generally has recommended, and will continue to recommend, voting case-by-case on certain equity-based compensation plans as evaluated using its equity plan scorecard ("EPSC") approach, which evaluates (i) plan cost, (ii) plan features, and (iii) grant practices. For 2017, ISS added to its list of problematic plan features dividends becoming payable before the award vests. Other plan features ISS continues to view as being problematic are:

- Automatic single-triggered award vesting on a change in control,

- Discretionary vesting authority,

- Liberal share recycling on various award types, and

- Lack of minimum vesting period for grants made under the plan.

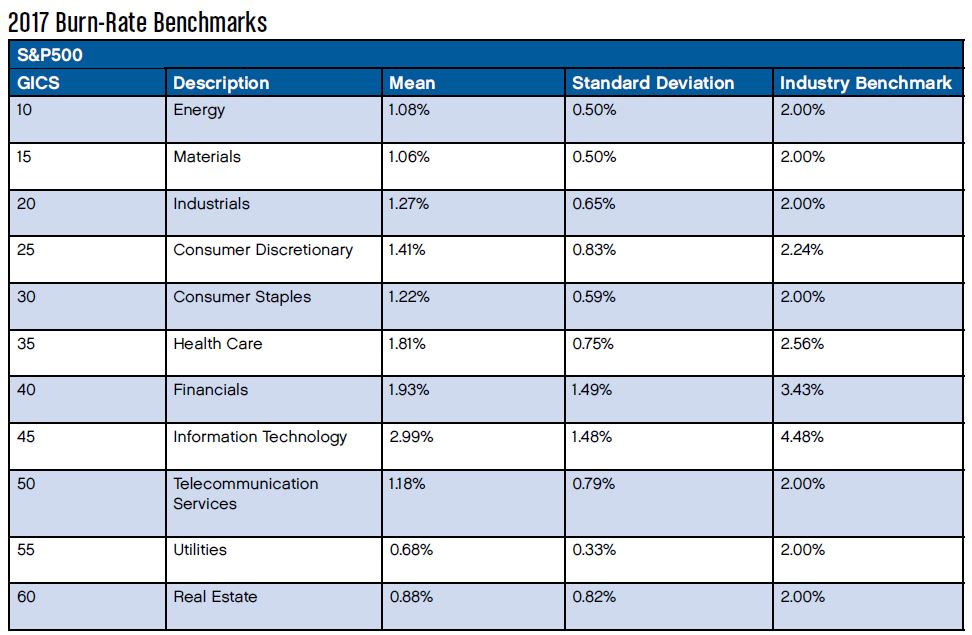

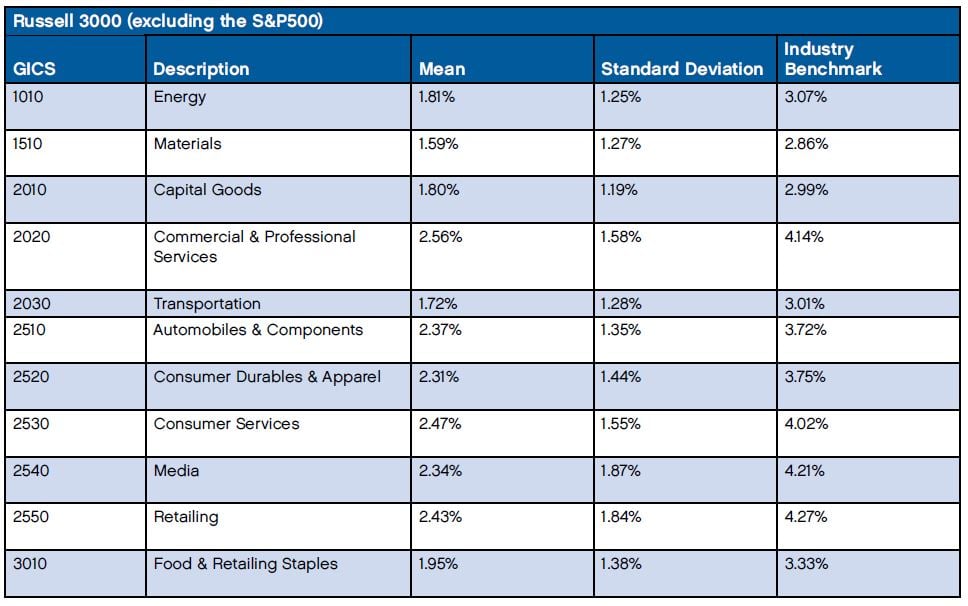

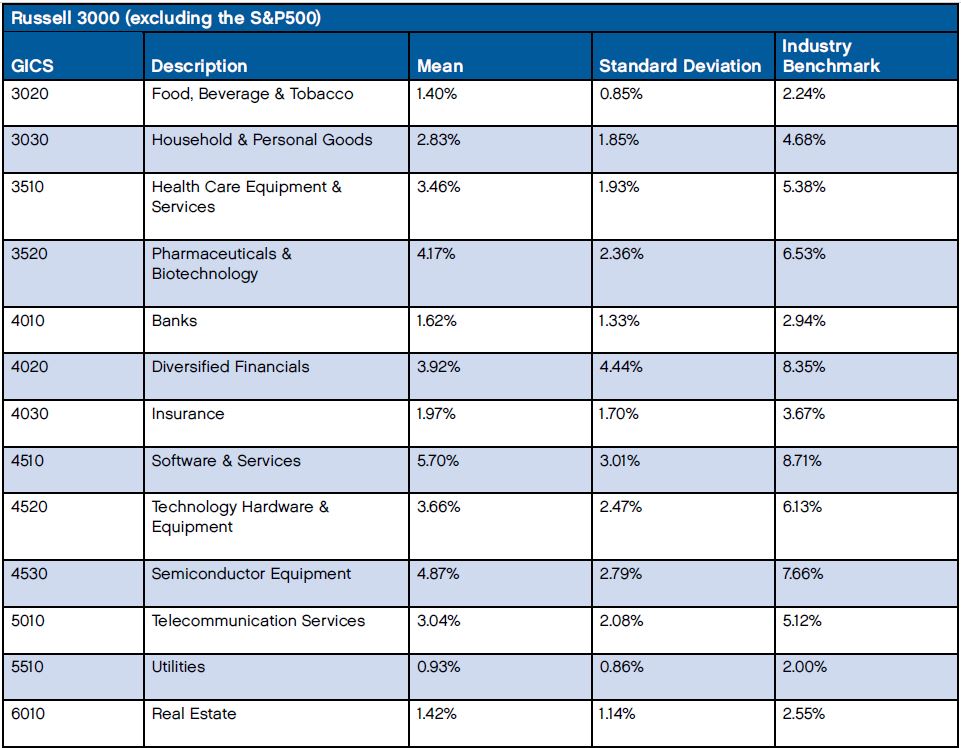

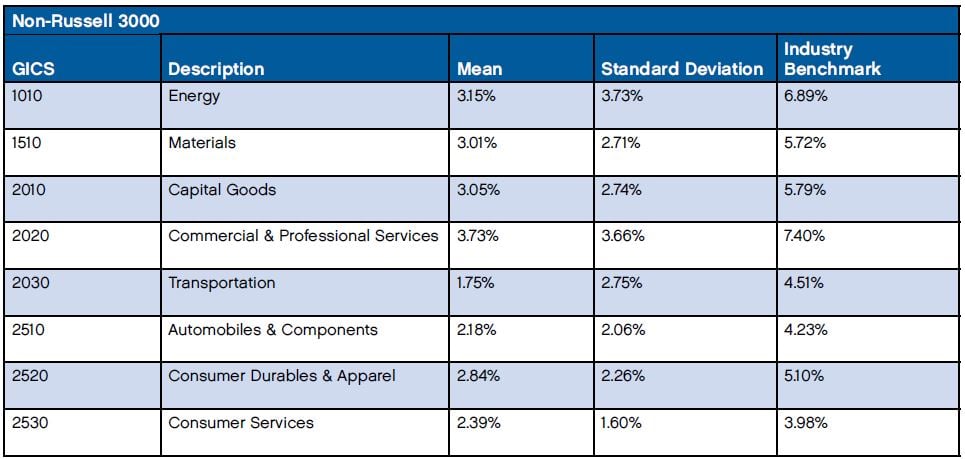

The plan cost and grant practices analyses under ISS's EPSC approach remain unchanged from 2016, except for updates to its burn-rate benchmarks. The updated 2017 burn-rate benchmark tables are included at the end of this update.

ISS will continue its historical practice of voting against an equity plan proposal if, according to ISS's analysis, the combination of plan cost, plan features, or grant practices indicates that the plan is not in the shareholders' interests or if any of the following factors apply:

- Awards may vest in connection with a liberal change in control definition,

- The plan would permit repricing or cash buyout of underwater options without shareholder approval,

- The plan is a vehicle for problematic pay practices or significant pay-for-performance disconnect (as evaluated by ISS), or

- Any other plan features are determined by ISS to have a significant negative impact on shareholder interests.

Amending Cash and Equity Plans

ISS's new general recommendation is to vote case-by-case on amendments to cash and equity incentive plans. ISS generally recommends voting for proposals to amend executive cash, stock, or cash and stock incentive plans if the proposal:

- Addresses administrative features only, or

- Seeks approval for section 162(m) purposes only, and the plan administering committee consists entirely of independent outsiders (as determined by ISS).

ISS recommends a vote against proposals to amend cash, stock, or cash and stock incentive plans if the proposal seeks approval for Internal Revenue Code section 162(m) purposes only and the plan administering committee does not consist entirely of independent outsiders (as determined by ISS).

ISS recommends voting case-by-case on all other proposals to amend cash incentive plans, including plans presented to shareholders for the first time after the company's IPO or proposals that bundle material amendments other than those for section 162(m) purposes.

ISS recommends voting case-by-case on all other proposals to amend equity incentive plans. It will consider the following in making this determination:

- If the proposal requests additional shares or the amendments may potentially increase the transfer of shareholder value to employees, the recommendation will be based on the EPSC evaluation as well as an analysis of the overall impact of the amendments (with heavier emphasis on the EPSC evaluation),

- If the plan is being presented to shareholders for the first time after the company's IPO, whether or not additional shares are being requested, the recommendation will be based on the EPSC evaluation as well as an analysis of the overall impact of any amendments (with heavier emphasis on the EPSC evaluation), and

- If there is no request for additional shares and the amendments are not deemed to potentially increase the transfer of shareholder value to employees, then the recommendation will be based entirely on an analysis of the overall impact of the amendments, and the EPSC evaluation will be shown for informational purposes.

In the 2016 proxy season, ISS made some surprising voting recommendations when it recommended voting against an amended plan, but would have recommended voting for the same exact plan if it had been in the form of a new plan rather than an amended plan. Although not addressed by ISS in its 2017 Guidelines or other written policies, in certain instances ISS conducts a "qualitative override" to plan amendments, which "qualitative override" does not apply to new plans. The "qualitative override" allows ISS to recommend voting against an amended plan that contains a change disfavored by ISS, such as a reduction in minimum vesting requirements, even if such change, when evaluated in the context of the entire amended plan under ISS's EPSC approach, would otherwise result in a recommendation to vote for such plan. Despite the potential to receive an arbitrary vote recommendation, a company should carefully consider the long-term implications of modifying its intended equity or incentive plan decisions to meet changing expectations imposed by ISS.

Shareholder Ratification of Director Pay Programs

ISS will generally recommend voting case-by-case on management proposals seeking ratification of non-employee director compensation. ISS lists the following factors to consider when making this determination:

- If the equity plan under which non-employee director grants are made is on the ballot, whether or not it warrants support, and

- An assessment of the following qualitative factors:

- the relative magnitude of director compensation as compared to companies of a similar profile,

- the presence of problematic pay practices relating to director compensation,

- director stock ownership guidelines and holding requirements,

- equity award vesting schedules,

- the mix of cash and equity-based compensation,

- meaningful limits on director compensation,

- the availability of retirement benefits or prerequisites, and

- the quality of disclosure surrounding director compensation.

Equity Plans for Non-Employee Directors

ISS has recommended, and will in 2017 continue to recommend, voting case-by-case on compensation plans for non-employee directors. For 2017, ISS added to its list of factors considered when making the determination the presence of any egregious plan features (such as an option repricing provision or liberal change in control vesting risk). The following factors remain unchanged from 2016:

- The total estimated cost of the company's equity plans relative to industry/market cap peers, measured by the company's estimated Shareholder Value Transfer (which is measured using a model that assesses the amount of shareholders' equity flowing out of the company to employees and directors) based on new shares requested plus shares remaining for future grants, plus outstanding unvested/unexercised grants, and

- The company's three-year burn rate relative to its industry/market cap peers.

ISS also changed its voting recommendation for director stock plans that exceed the plan cost or burn-rate benchmarks when combined with employee or executive stock plans. In 2016, ISS recommended voting for such plans as long as the plan set aside a relatively small number of shares and met certain qualitative factors. For 2017, however, ISS recommends voting case-by-case on director stock plans exceeding the plan cost or burn-rate benchmark when combined with employee or executive stock plans. ISS indicates that the following qualitative factors should be considered when making this determination:

- The relative magnitude of director compensation as compared to companies of a similar profile,

- The presence of problematic pay practices relating to director compensation,

- Director stock ownership guidelines and holding requirements,

- Equity award vesting schedules,

- The mix of cash and equity-based compensation,

- Meaningful limits on director compensation,

- The availability of retirement benefits or prerequisites, and

- The quality of disclosure surrounding director compensation.

What to Do

ISS's new voting guidelines should not change any company's practices or plans; however, companies may want to reconsider their approach to the shareholder engagement process and certain other things, such as how they disclose their executive and director incentive and equity plans and the messaging that is conveyed through their proxy statements.

2017 Burn-Rate Benchmarks